You have decided to invest in mutual funds. You have selected the best mutual funds for you. You have also decided whether you want to invest lump sum or through Systematic Investment Plans (SIPs) or STPs.

Live TV

Loading...

There is one decision that you are yet to make. Which investment option to select?

Growth or dividend or dividend re-investment?

In this post, we will discuss the difference between the three options. We will also discuss various elements that can influence investors’ preference for one of the options. First, let’s see what these options are all about:

What are Growth and Dividend options in Mutual Funds?

The choice between the dividend reinvestment and growth options depends upon investment horizon, applicable income tax slab and tax treatment of capital gains and dividend income.

Please note that the fund portfolio is exactly the same for growth, dividend or dividend reinvestment plans.

How Mutual Fund Investments are taxed?

Mutual fund taxation keeps changing. Till FY2018, long term capital gains and dividends from equity mutual funds were exempt from income tax.

However, Budget 2018 changed everything. Now, even LTCG from the sale of equity funds and dividends from equity funds are taxed.

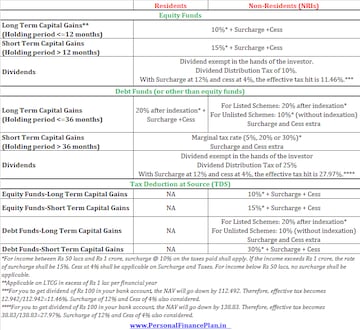

Here is how the mutual fund taxation looks like. I have included the rates for both residents and non-residents.

Now, the tax treatment of capital gains and dividends is one of the deciding factors between choosing growth or dividend or dividend re-investment option.

If the tax regime provides favourable tax-treatment to one kind of income (capital gains or dividends), you must invest in a more tax-friendly option.

If capital gains get better treatment, Growth option is better.

If dividends get better tax treatment, Dividend (or reinvestment) option is better.

By the way, if there were no tax difference, there wouldn’t be much difference between growth and dividend because you can always sell your units to generate income (instead of waiting for the dividend). Alternatively, whatever dividend you generated could be reinvested. Unfortunately, that’s not the case. And that forces us to do some work.Dividends or Capital gains?

There are two kinds of income on which a person may be required to pay tax.

Dividend income or Capital gains.

Under a growth fund, all income will be in the form of capital gains (since no dividend is paid out). Under the dividend/dividend re-investment option, income will be in form of both dividend and capital gains.

If a mutual fund pays the dividend, its NAV will go down by the same amount and will reduce potential capital gains on the sale of units. In fact, if you select the dividend option, the NAV of the fund will go down by more than the amount received (or re-invested) as dividend because of Dividend Distribution tax (DDT).

As per the current tax laws, the dividend received from mutual funds is exempt from tax in your hands. However, the fund house deducts the TDS (or DDT) before paying the dividend to you. And that explains why the NAV falls more than the dividend received. For more on how DDT is calculated, refer to this post.

What to do in case of Equity Mutual Funds?

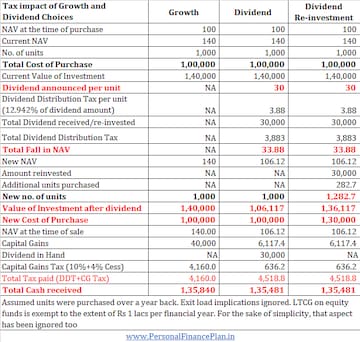

Suppose an equity MF unit cost you Rs 100 at the time of purchase. After 2 years, NAV of the same unit has risen to Rs 140. Subsequently, the MF scheme announces a dividend of Rs 30 (for dividend and dividend reinvestment plans). The investor sells the units soon after. Exit load implications not considered.

Dividend option: The MF scheme announces a dividend of Rs 30, you get a dividend of Rs 30 per unit (total dividend of Rs 30,000). Due to DDT, the NAV will fall to Rs 106.12. If you decide to sell MF units subsequently, your capital gains will be Rs 6.12 per unit (total of Rs. 6,117.4). After capital gains tax, your net in-hand cash is Rs 1,35,481.

Growth option: Since there are no dividend payments and you sell off the unit, you will make capital gains of Rs 40,000. At LTCG tax of 10.4 percent (includes 4 percent cess), your CG tax liability is Rs 4,160. Your net cash received is Rs 1,35,840 (higher than the dividend option).

Dividend re-investment: No payout will be made to the investor. Dividend (declared and not paid out) will be used to buy additional units (Additional units = Dividend declared/Revised NAV i.e. 30,000/106.12=282.7 units). In this case, dividend is not paid and all the cash inflow will be only at the time of redemption. After accounting for LTCG tax, net cash received is Rs 1,35,481.

In case of equity funds, short term capital gains (less than 1 year) are taxed at 15 percent while long term capital gains are taxed at 10 percent (before cess & surcharge). Dividends are taxed at about 11.46 percent. Moreover, LTCG on equity funds is exempt from tax up to Rs 1 lac per financial year. No such relief for Dividends. If you incur a loss on sale of equity funds, you can use it to set off your capital gains. No such thing for dividends.

Clearly, in case of equity funds, capital gains get more benign tax treatment. Therefore, in the case of equity funds, growth option is a far better choice.

Many investors invest in dividend option of equity mutual funds for regular income. It is not a good choice. Why? Refer to this post.

You may argue that the STCG on equity funds is 15 percent. Effective impact of DDT is much lower. You are right. However, equity investments are not really for the short term. Moreover, dividend (or its quantum) or are not guaranteed. In my opinion, this debate is meaningless.

In case of equity funds, Growth option is a clear winner.

I do concede there may be merit in considering dividend options of arbitrage funds (because they behave like debt funds but are taxed like equity funds).

One aspect that I have not considered in the above illustration, is that of surcharge on capital gains. Surcharge at 10 percent or 15 percent on capital gains is applicable if your income exceeds Rs 50 lacs or Rs 1 crore respectively. Do note surcharge at 12 percent is always applicable on dividend distribution tax (irrespective of income tax slab). If surcharge is applicable to capital gains, the tax difference between growth and dividend will almost vanish. In fact, if your annual income is more than Rs 1 crore, the dividend option will be more tax-friendly. However, we have to see applicability too.

Moreover, we have to also consider LTCG exemption of Rs 1 lac and flexibility to set off capital losses, and potential set off against the minimum exemption limit of Rs 2.5 lakh (or as the case may be). Dividends offer no such relief. My vote goes to Growth for equity funds.

What to do in case of Debt Mutual Funds?

Again, the tax treatment is a key factor.

In case of debt funds, short term capital gains (holding period up to 3 years) are taxed at your slab rate. If you are in 5 percent tax slab, you have to pay 5 percent. If you are in 20 percent and 30 percent tax bracket, your STCG on debt funds will be taxed at 20 percent and 30 percent respectively. Cess extra. Surcharge if applicable.

LTCG (holding period above 3 years) is taxed at 20 percent after accounting for inflation.

The dividend distribution tax is 25 percent in case of debt funds. Given the way DDT calculation works and including cess and surcharge, your effective tax hit is 27.97 percent.

In the case of debt funds, the choice is quite clear.

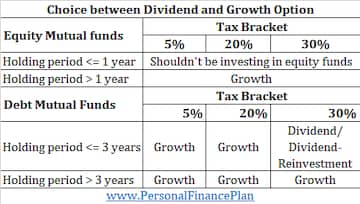

If you are in 5 percent or 20 percent tax brackets, the Growth option is a clear winner (whether for short term or long term). This is because DDT is way higher.

If you are in 30 percent tax bracket and you are investing for less than 3 years, the Dividend/dividend re-investment option is a better choice (since your capital gains will be taxed at over 30 percent. DDT is lower).

If you are in 30 percent tax bracket and you are investing for more than 3 years (or you are not sure if you will need this money in 3 years), Growth option is a better choice (since Capital gains are taxed at only 20 percent after indexation).

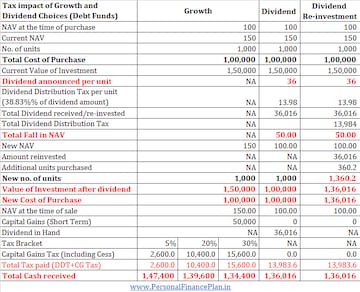

In the below tabulation, I have showed the workings for short term capital gains. I have chosen the quantum of dividend in a way that Capital gains tax liability does not arise in case of dividend options.

You can see that if you plan to sell your debt funds investments before 3 years, your tax slab becomes a key determinant. If you are in the highest tax bracket, you will find dividend option better. Others will benefit from the Growth option.

If you have been holding for over 3 years (rather your investment horizon is less more 3 years), then Tax on LTCG (20 percent after indexation) is far better than DDT. So, Growth is a clear winner.

PersonalFinancePlan Take

Growth option is a clear winner in most cases. Here is a crisp recap of what you should do. From the perspective of decision making, replace “holding period” with “investment horizon”.

Deepesh Raghaw is a SEBI registered investment advisor and founder of www.PersonalFinancePlan.in. You can read the original article here.

First Published: Feb 19, 2019 10:09 AM IST

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!

Supreme Court says it may consider interim bail for Arvind Kejriwal due to ongoing Lok Sabha polls

May 3, 2024 4:57 PM

10% discount on fare on Mumbai Metro lines 2 and 7A on May 20

May 3, 2024 2:40 PM