homemarket Newsstocks NewsHDFC Bank sheds ₹1.1 lakh crore in m cap after dropping most in three years: Should you buy?

HDFC Bank sheds ₹1.1 lakh crore in m-cap after dropping most in three years: Should you buy?

HDFC Bank reported a net profit of ₹16,372 crore, marking a sequential increase of 2.5% and yearly rise of 33.5%. It is important to note that HDFC Bank merged with Housing Development Finance Corp (HDFC) in June 2023.

Shares of HDFC Bank on Wednesday, January 17, erased ₹1.1 lakh crore in market capitalisation after posting biggest single-day fall in three years. The shares of the lender declined following the release of the company's third quarter results.

Brokerages offered varied perspectives on the HDFC Bank's performance.

The bank reported a net profit of ₹16,372 crore, marking a sequential increase of 2.5% and a yearly rise of 33.5%.

It is important to note that HDFC Bank merged with Housing Development Finance Corp (HDFC) in June 2023.

Here's a table summarising the target prices provided by various brokerages after HDFC Bank's Q3 results:

| Brokerage | Recommendation | Target Price (₹) |

|---|---|---|

| Bernstein | Outperform | ₹2,200 |

| Morgan Stanley | Overweight | ₹2,110 |

| Jefferies | Buy | ₹2,000 |

| HSBC | Buy | ₹1,950 (reduced from 2,080) |

| InCred | Add | ₹2,000 |

| DAM Capital | Buy | ₹2,000 |

| Motilal Oswal | Buy | ₹1,950 |

What do brokerages say?

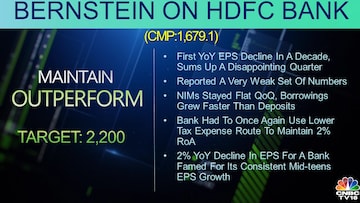

Brokerage firm Bernstein has an 'Outperform' recommendation on the lender, setting a target of ₹2,200 per share. It acknowledged the bank's weak set of numbers, noting the first year-on-year earnings per share (EPS) decline in a decade.

Flat Net Interest Margins (NIMs) quarter-on-quarter (QoQ) and a 2% year-on-year decline in EPS were highlighted by the firm. The use of lower tax expenses to maintain a 2% Return on Assets (RoA) was mentioned.

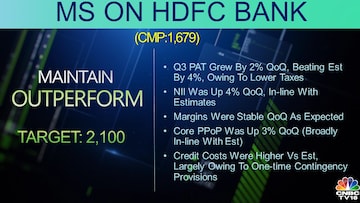

Morgan Stanley (MS), with an 'Overweight' recommendation and a target of ₹2,110 per share, positively noted a 2% QoQ growth in Profit After Tax (PAT), beating estimates by approximately 4%.

It described the Net Interest Income (NII) as in line with estimates and stable margins QoQ. A stable core Pre-Provision Operating Profit (PPoP) and higher credit costs due to one-time contingency provisions were observed by the brokerage.

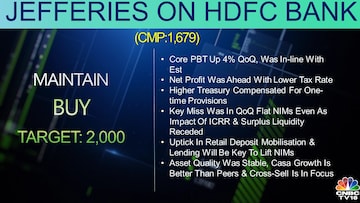

Jefferies recommended 'Buy', setting a target of ₹2,000 per share.

It commended the bank's core Profit Before Tax (PBT) growth and net profit exceeding estimates with a lower tax rate. An uptick in retail deposit mobilisation and lending was emphasised as crucial to lifting Net Interest Margins (NIMs).

Stable asset quality and the importance of retail growth were acknowledged by the brokerage.

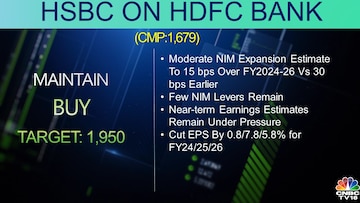

HSBC, maintaining a 'Buy' recommendation but reducing the target to ₹1,950 from ₹2,080 per share, moderated the Net Interest Margin (NIM) expansion estimate from 30 bps to 15 bps over FY24-26.

It reduced near-term earnings estimates, citing pressure.

Despite lowering the target, HSBC maintained a positive stance on HDFC Bank.

InCred recommended an 'Add,' with a target of ₹2,000 per share.

It praised the bank's healthy Profit After Tax (PAT) in Q3 amid a steady quarter-on-quarter (QoQ) margin. The brokerage further highlighted the utilisation of treasury gains for a contingent provision and cautious management of deposit growth.

InCred expressed confidence in credit growth and manageable deposits.

DAM Capital, with a 'Buy' recommendation and a target of ₹2,000 per share, noted a 10% beat in Q3 earnings due to a lower tax rate and mark-to-market (MTM)/trading gains.

It emphasised steady core profitability and the creation of a contingency buffer using better treasury gains. The increase in provisions was acknowledged, but DAM Capital maintained a favourable view on valuations.

Motilal Oswal has reiterated its buy rating on HDFC Bank stock with a target price of ₹1,950.

The brokerage firm underscored that HDFC Bank reported in-line earnings led by healthy other income and steady loan growth.

What should investors do?

The brokerages present a diverse range of perspectives on HDFC Bank's Q3 results, reflecting both positive and cautious sentiments.

However, speaking of market experts, Ashutosh Mishra, Head-Research, Instl Equitiesm, Ashika Stock Broking, said that the current valuation is 'quite compelling' particularly when considering not only HDFC's standalone performance but also the collective performance of its subsidiaries post-merger.

Mishra emphasised the successful execution of the substantial merger, noting the absence of significant negative impacts.

According to him, this positions HDFC Bank as a "screaming buy" at its current level, offering substantial potential gains over the next two to three years.

Deven Choksey, MD, DR Choksey Finserv, highlighted the role of growth in influencing stock prices.

For Choksey, the current results present an opportunity to invest in HDFC Bank at corrected and lower levels.

He views this as a meaningful buying opportunity, foreseeing potential gains ranging from 25-30% going forward

Stock performance

The US-listed shares of HDFC Bank fell 6.7% overnight.

This is the biggest single-day drop seen by the shares listed on the New York Stock Exchange (NYSE) since April 2022, when they had declined 7.5%. It must be noted that HDFC Bank commands over 14% weightage on the Nifty 50 index, which is the highest among the constituents.

(Edited by : Amrita)

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!