JPMorgan maintains 'overweight' position on BPCL and IOCL-Here's why

JPMorgan has adjusted its target multiples for enterprise value (EV) to earnings before interest, taxes, depreciation, and amortization (EBITDA) from five times to six times for all three stocks.

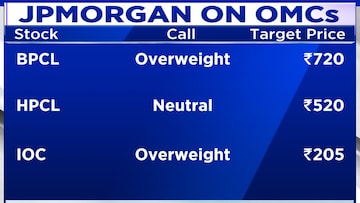

State-owned oil marketing companies (OMCs) are in focus after a recent note from JPMorgan. The global investment major has raised target prices for three major players: Bharat Petroleum Corporation Ltd (BPCL), Indian Oil Corporation Ltd (IOCL), and Hindustan Petroleum Corporation Ltd (HPCL).

In its analysis, JPMorgan highlights the impact of fluctuating crude oil prices on the performance of these companies. In January, there was a noticeable increase in crude oil prices, followed by a further rise of approximately $5.50 per barrel in February. This upward trend initially boosted stock prices.

They say crude is still at December quarter averages. In addition, the fear is that diesel or petrol prices will be reduced, although that hasn't happened yet, which is protecting their marketing margins. JPMorgan also added that the consensus EPS estimates for FY24 are still very low. Hence, there is a possibility of an upside.

As a result, JPMorgan suggests that unless there are significant changes in crude oil prices or retail fuel pricing strategies, the outlook for OMCs may remain stable. They anticipate a continued upward bias in stock prices for these companies.

JPMorgan has adjusted its target multiples for enterprise value (EV) to earnings before interest, taxes, depreciation, and amortization (EBITDA) from five to six times for all three stocks. Additionally, they maintain a preference for BPCL, followed by HPCL, and have accordingly revised their target prices: BPCL to ₹720, HPCL to ₹520, and IOCL to ₹205.

JPMorgan continues to recommend an 'overweight' position on BPCL and IOCL within investment portfolios, reflecting their positive outlook on these companies' future performance.

(Edited by : Ajay Vaishnav)

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!

Prajwal Revanna Sexual Assault Case: Activist raises concerns over political interference, delayed investigation in the matter

Apr 30, 2024 10:17 PM

Lok Sabha Election 2024: Baramati election outcome will decide the future of Pawar dynasty, says expert

Apr 30, 2024 10:08 PM

Lok Sabha elections 2024: Baramati to Mainpuri, key battles in phase 3

Apr 30, 2024 7:01 PM