"To do nothing at all is the most difficult thing in the world, the most difficult and the most intellectual." When Oscar Wilde said these words, he was not referring to investing, but it applies equally well to investing, especially in volatile periods.

With various stock indices down

(Nifty down 11 percent, Nifty SmallCap down 30 percent) and the accompanying new cycle of gloom and doom, there is a natural tendency to "want to do something"- which usually means giving into fear and selling available investments or to greed and buying more.

However, academic and practitioner research reveal two major things:

While the first has been well known for long, it is the second that we find very interesting. The popular corollary of it is investing based on past three year or five year returns and then expecting the next three to five year returns to be the same.

Based on a research paper titled “Expectations of Returns and Expected Returns”, by Shleifer and Greenwood, both professors at Harvard University, we come to three conclusions on investor behavior and how past returns of funds and indices affect decision making.

Figure 1: Most investor surveys show similar expectations regardless of the population being surveyed. Source: Greenwood and Shleifer (2014)

Figure 1: Most investor surveys show similar expectations regardless of the population being surveyed. Source: Greenwood and Shleifer (2014)No wonder more retail investment accounts are opened at the last stages of a market rally when the past three to five year returns look really good, then at the beginning.

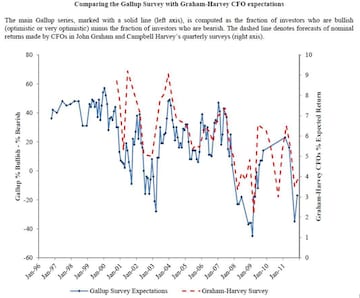

Figure 2: Investors extrapolate based on the past to form return expectations. Source Greenwood and Shleifer (2014).

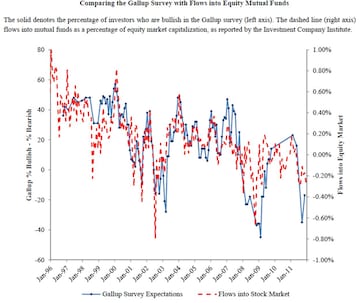

Figure 2: Investors extrapolate based on the past to form return expectations. Source Greenwood and Shleifer (2014). Figure 3: Investors act based on their return expectations in form of putting or withdrawing money from equity mutual funds. Source Greenwood and Shleifer (2014).

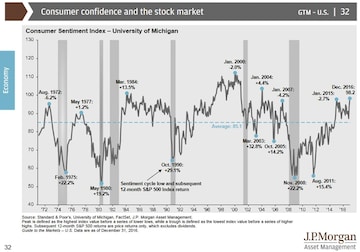

Figure 3: Investors act based on their return expectations in form of putting or withdrawing money from equity mutual funds. Source Greenwood and Shleifer (2014).This would all still be fine if the resulting investments worked out. However, this chart from JP Morgan shows that average investors are quite bad at guessing the direction of returns. So, when we expect higher returns (and have invested based on that belief) the actual returns tend to be low and when we have withdrawn money based on our low sentiment and we expect low future returns, the returns tend to be higher. This is also consistent with the negative correlation between the actual returns and the expectations of those returns formed by Greenwood and Shleifer.

Figure 4: Investor expectations and future performance tend to be negatively related! Source: JP Morgan Asset Management, Guide to the Markets 1Q 2017.

Figure 4: Investor expectations and future performance tend to be negatively related! Source: JP Morgan Asset Management, Guide to the Markets 1Q 2017.So what should we do?

But does this apply to the Indian stock market?

Astute readers will point out that the studies cited were not conducted on the Indian markets and question the validity of applying them here. We agree with these readers and would respond that while we do not know if the Indian markets will behave exactly the same, but human investing behavior is more likely to at least rhyme if not repeat itself. We would also point to the many academic studies that find more similar market behavior across the world than dissimilar. One such study is "Value and Momentum Everywhere" (Asness et al. , 2013) that finds that the same investing strategies or factors such as value and momentum that were initially tested in the United States on individual stocks have similar performance across multiple asset classes such as equities, bonds, currencies and commodity futures, and in other countries such as United Kingdom, continental Europe, and Japan.

Conclusion

We will explore more behavioral biases in upcoming articles and why the returns generated by the average investors may not be close to the index returns - in part due to our impulse to time re actively.

So, practice doing this very important and difficult thing - do nothing.

Apurv Jain is a visiting researcher at Harvard Business School working on using Big Data and AI in investing. He is an investor in and advisor to Kuvera.in: India’s first completely free Direct Mutual Fund investing platform.

References

First Published: Oct 17, 2018 11:30 AM IST

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!