homeeconomy NewsRising US yields, geopolitical shifts and RBI's hawkish stance challenge Indian bonds, says Morgan Stanley

Rising US yields, geopolitical shifts and RBI's hawkish stance challenge Indian bonds, says Morgan Stanley

The rise in US yields has taken center stage, surging by approximately 130 basis points since May. This unexpected development has sent shockwaves through the Indian and Asian bond markets.

Chetan Ahya, Chief Asia Economist at Morgan Stanley expects the Reserve Bank of India to begin cutting rates from the second quarter of calendar year 2024.

"We are expecting just about a 50-bps cut. So, it will be a shallow rate-cut cycle," he told CNBC-TV18.

Ahya also shared his thoughts on the bond market and geopolitical changes in the Middle East.

Bonds and currencies in India and across Asia have encountered unforeseen challenges. The primary concern is the significant increase in US yields, which has surged by approximately 130 basis points since May.

Even though there has been a slight reduction in US yields, recent geopolitical changes in the Middle East have raised fresh concerns about oil prices, which, in turn, affect Asian bonds.

Below is the verbatim transcript of the interview:

Q: We have a plateful over here in terms of issues. But first, let me begin with the US bond yields. This time Asia, according to your report is not going to be impacted much.

A: Yes, that is right. I think the bulk of the rise in real rates that we have seen in the US has been driven by the fact that term premiums have gone up, and market expectations on the Fed policy rate hikes have not been much. So that is one important difference in terms of the rise in the US yields this time.

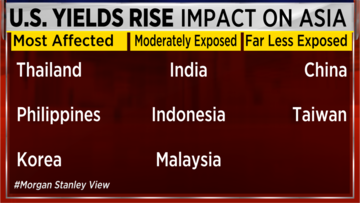

The second is that Asia's inflation outlook has been still quite comfortable. We are expecting that Asia is going to see 80% of the region’s central banks having inflation within their comfort zone or closer to target by the end of this month, when you get the data for the September quarter, everybody's inflation will have looked like it's within central bank's comfort zone. So, Asia does not have that big an inflation problem and so usually the way we think about this dynamic when US rates are going up is the fact that whether Asian central banks have their policy setting in a way that the macro stability indicators like inflation and current account balance are in a good position.

And when you try to answer that question, the answer is yes. Most of the countries in the region except for the Philippines have inflation and current account balances in a shape that central banks do not have to take up interest rate hikes.

And so, this is the main thought process behind which we are saying that Asia’s macro stability indicators are in good shape. We do not think central banks have to respond to this rise in US interest rates with higher policy rates.

Q: They may not do it with higher policy rates, but will they have to postpone rate cuts? I mean, can you really cut, say Indian repo rates, if the US yields are still climbing? Never mind even if the Fed has stopped; if the yields are climbing, will that be a bit of a challenge for the currency, and therefore will RBI desist from rate cuts?

A: That is right. We do not think that the central banks in the region will be able to cut interest rates when the US rates are rising up or the dollar is strengthening too much with Fed rate hike expectations going up. That is the reason why we have most of the region's central banks, which are about to be able to cut rates will be delayed till Q2 of next year. So that is the quarter ending June 2024 because we also expect that by that time Fed would have indirectly or directly indicated that they are not taking up more rate hikes and that they are actually about to cut interest rates.

So, we will need confirmation from the Fed that the Fed is done with this tightening cycle and it's about to embark on an easing cycle for Asian central banks to also be able to cut rates.

But the reason why we are thinking about some modest rate cuts in the region is that you will have a dynamic where inflation would have decelerated quite a lot and real rates would have been rising. That would be away from the policy stance that various central banks would have is that real rates would have implied that you are tightening monetary policy when it may not have been warranted.

Q: I will come back to Asia and India, but what is Morgan Stanley’s house view on US yields itself? This move in the 10-year from 3.5% in May-June, all the way to 4.85% was quite unexpected. And there has been a kneejerk 20 basis fall. So is a significant retracement expected, or is the medium-term range likely to be towards 5 because there is fiscal oversupply?

A: We are expecting rates to moderate from here and our thought process is that if you break up the 10-year bond yield trends into policy rate expectations and term premium. Both those aspects, we think, will support 10-year bond yield to go lower.

But the most important driver to our lower rates forecast is that the Fed will be cutting rates in the next calendar year by about 75 to 100 basis points. And that is what will create that environment for US 10-year rates to go down.

So, we have been of that view, and you are right, the recent rise was a surprise, and it was not in our forecast. But our US rates team is still maintaining that the trajectory of the 10-year bond yield is downward, closer to four-handle rather than staying at 5%.

Q: Four-handle, that is still a long way if we have to get closer to 4%, but coming back to India, how do you assess the Reserve Bank's response to the monetary policy? Why would they announce such an important step like an OMO, an open market sale that has pushed up yields considerably? Should that be read as a defense against US yields?

A: Yes, I would think so. I think the way we are seeing various Asian central banks - some of them are explicit like BoK, which mentions the Fed policy path and what is happening to the US rates. And RBI has been sort of more focused on the domestic inflation.

But it's very clear that somewhere in the back of the mind, the developments in the US rates and the Fed policy outlook are weighing on the RBI’s mind as well, and in an environment where oil prices had been rising, at least at the time when monetary policy decision got taken. They would have to consider the fact that you have a combination of higher US rates, higher dollar, and higher oil prices weighing on the inflation outlook.

So, they didn't want to sound in any way indicative that they are done, and they are going to cut rates because that will ease financial conditions and that will risk that the currency will depreciate, and I think that's really the main driver behind RBI’s increased hawkishness.

We do not think that the underlying inflation dynamic in India is right now warranting that shift and hawkishness but it's the outlook of that inflation affected by this, potential dollar rises, and higher oil is that has weighed on RBI’s mind.

Q: I am not trying to ask you your view on the new geopolitical problem in the Middle East, the Israel-Hamas war, but will Asia have to struggle with higher crude prices? Is that one of your base cases?

A: Right now, our oil analyst is not forecasting oil prices to rise meaningfully. Our forecast is that oil prices will average around $95/bbl in the fourth quarter of this year, and then head towards $85/bbl next year.

So, we are not expecting all prices to go up in our base case. But if it does go up because of these geopolitical tensions, it will definitely complicate the monetary policy management in the region.

And so, in that scenario, while I mentioned our base case, we are not expecting rate highs; in fact, we are expecting rate cuts to be happening, though in a delayed manner. In this risk scenario, where oil prices shoot up, we will see that there is a possibility that some of the central banks may have to pick up a rate hike.

Q: What is your RBI rate cut date?

A: We are forecasting a rate cut in the second quarter of 2024, and we are expecting just about a 50-bps cut. So, it will be a shallow rate-cut cycle.

Q: When you say second quarter you mean second calendar quarter, right? April-May-June?

A: That is right, the April to June quarter.

Q: On growth, the US yields are high, we hear about problems in the commercial real estate and with the 10-year yields, with the term premium also rising is there a chance that US growth and therefore global growth gets impacted. What would your take be for India if the global impulses are going to be weak?

A: First, on the US, we are expecting growth to slow from this quarter itself. There are a few things that are going on in the US. One, real rates are rising, and so monetary policy is gradually tightening. Second, we do not think we will get as much fiscal support and so fiscal impulse is not going to be positive like it was in the last 12 months. Third, there is going to be the student loans, repayment that will burden the consumers. And finally, the excess saving stock for the bottom 20% has exhausted. So, we are expecting consumption slowdown and overall growth slowdown in the US. In the context, this recent real rate rise has only added to that downward pressure because the US economy is funded to a large extent with long tenure borrowing. And therefore, we think that case that we have in our base case that there will be a slowdown is only getting more confirmed. Now, as far as India is concerned, this may not be a bad thing. So as long as the US is slowing, but not going into a deeper recession, it will be good for the region and India in the sense that it takes off this pressure of dollar rise and US higher rates but brings it down into a situation where you don't have a big downside to exports growth. So soft landing in the US even if it may be a deeper slowdown, it’s fine as long as you do not get a deeper recession.

Q: So, Indian growth, what is your number now?

A: We are at 6.4% for the current financial year. And the next financial year we are at around the same number – 6.5% on an average.

(Edited by : Shweta Mungre)

First Published: Oct 11, 2023 9:41 PM IST

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!

Repolling underway at one polling booth in Chamarajanagar LS segment in Karnataka

Apr 29, 2024 10:32 AM

2024 Lok Sabha Elections | What does a low voter turnout indicate for NDA and I.N.D.I.A Bloc

Apr 29, 2024 5:48 AM

'Borrowed' leaders: Congress hits out at AAP for not fielding their own candidates in Punjab

Apr 28, 2024 9:53 PM

EC asks AAP to modify election campaign song and Kejriwal's party is miffed

Apr 28, 2024 9:25 PM