homeearnings NewsWill strong deal wins result in better guidance from TCS, Infosys and peers?: IT Earnings Preview

Will strong deal wins result in better guidance from TCS, Infosys and peers?: IT Earnings Preview

The highlight of the quarter will be the deal wins. Large deals have been particularly robust during the quarter. Infosys, for example, signed a large deal with Liberty Global, TCS with Jaguar Land Rover, HCLTech with Verizon etc.

Technology services providers TCS Ltd., Infosys Ltd., Wipro Ltd. and others will be in focus for the rest of the month as they begin reporting their September quarter results, starting with TCS on October 11.

The Nifty IT index has risen 7.5% in the July-September quarter, comfortably outperforming the Nifty 50 index, which rose only 1.6%. The outperformance has been driven by strong deal wins and expectations of demand revival in financial year 2025, as most analysts on the street have been projecting.

This time around, the focus will be on signs; commentary on whether the worst of the demand deterioration is over, whether there are greenshoots in demand, will growth recover in the second half of financial year 2024 and what is financial year 2025 looking like?

The September quarter appears to be a continuation of the weakness seen earlier. While there have been strong deal wins, there has been no deterioration in demand but no improvement either.

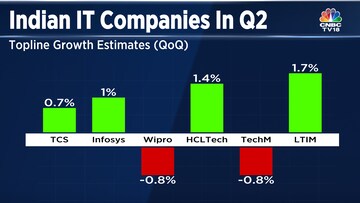

Infosys is likely to see another quarter of just 1% growth, while Wipro's revenue may decline for the third straight quarter. However, that number is likely to be within its guided range.

The highlight of the quarter will be the deal wins. Large deals have been particularly robust during the quarter. Infosys, for example, signed a large deal with Liberty Global, TCS with Jaguar Land Rover, HCLTech with Verizon etc.

Kotak Institutional Equities estimates Infosys to report Total Contract Value between $5.5 billion to $6 billion, well above the previous eight-quarter average of $2.4 billion. TCS may report deal value worth $12 billion, up 48 percent from last year.

The question to be asked though, is whether these large deals will be margin dilutive? For the September quarter, margins are likely to remain stable.

Some of the other factors to watch out for for specific companies:

On the valuation front, most of the companies on a financial year 2025 basis are trading below their three year average, but trading well above their pre-Covid three-year average.

| Company | Valuation (FY25 P/E) | Three-Year Average P/E | Pre-Covid Three-Year Average P/E |

| Infosys | 20x | 23x | 18x |

| TCS | 24x | 27x | 22x |

| Wipro | 17x | 20x | 15x |

| HCLTech | 19x | 20x | 14x |

| LTIMindtree | 26x | 30x | 17x |

| Tech Mahindra | 21x | 20x | 15x |

Kawaljeet Saluja, Executive Director & Head-Research, Kotak Institutional Equities told CNBC-TV18, “The numbers are going to be weak across all companies. The revenue growth will be fairly muted but the focus this quarter is going to be on the dealwins. Talking purely about the numbers, nothing much to look forward to in the quarter."

For more details, watch accompanying video

(Edited by : Hormaz Fatakia)

First Published: Oct 8, 2023 8:07 PM IST

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!

Telangana Lok Sabha elections 2024: Asaduddin Owaisi to Bandi Sanjay Kumar, a look at key candidates

May 11, 2024 3:32 PM

Lok Sabha elections 2024: Hyderabad to Kadapa, key seats in fourth phase

May 11, 2024 2:54 PM

Telangana Lok Sabha elections 2024: List of BRS candidates

May 11, 2024 1:55 PM