homebusiness Newscompanies NewsThis Hyderabad based cement company is looking to turn around years of underperformance

This Hyderabad-based cement company is looking to turn around years of underperformance

Orient Cement is also confident that the company will outgrow the industry by 200-300 basis points in the next financial year.

Orient Cement has always presented value to its shareholders, but has underperformed in terms of returns.

Shares of the CK Birla Group company have halved from where they were in October 2016.

The market is an important question - Will Orient Cement finally deliver returns for its shareholders? CNBC-TV18 travelled to the company's headquarters in Hyderabad and seek answers from Orient Cement's CEO and MD Deepak Khetrapal.

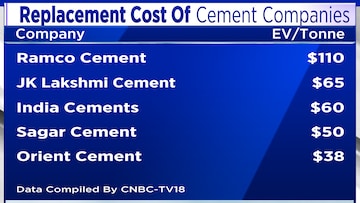

Let us fetch you some numbers. Replacement cost of a cement plant is nearly $100 per tonne. Orient Cement trades at $38 per tonne, which is a steep discount for an 8.5 MT integrated cement capacity company. Replacement cost is the amount of money spent to replace an asset of a company at the same or equal value.

Orient Cement's shareholding has had some of the biggest names from the investor faternity. The late Rakesh Jhunjhunwala also featured on that list till the September 2022 quarter. Also among shareholders is HM Bangur of Shree Cement, who has a stake of over 1 percent as of December 2022.

17 percent of the company's shareholding is owned by institutions with Mutual Funds like Franklin India Focused Equity Fund, Nippon Life India Trustee Ltd. and Aditya Birla Sun Life Trustee Pvt. Ltd. featuring in that list.

Despite a capacity of 8.5 MT, utilisation has scaled 75 percent only once in financial year 2019.

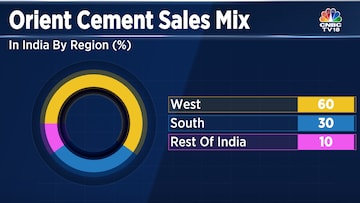

Bulk of their sales mix is concentrated in the West and South India. Both these regions have had their share of problems on overcapacity and on the pricing front.

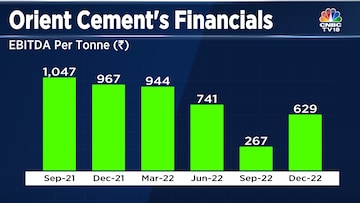

Orient Cement's financial performance has shown some improvement during the December quarter after hitting rock bottom in the September quarter. The management is also confident of a much improved performance in the results awaited. Operating profit per tonne also fell from Rs 1,000 earlier to the current Rs 600, but the management is confident of steady improvement hereafter.

The debt in books has been gradually coming down. Total debt as of last count was approximately Rs 400 crore.

CEO and MD Deepak Khetrapal said that EBITDA per tonne can improve by Rs 200-250 per tonne in financial year 2024, with possibilities of further upside if cement prices improve. He expects that to happen through premiumisation, cost savings, and higher volumes. Khetrapal is also confident that the company will outgrow the industry by 200-300 basis points in the next financial year.

Khetrapal also mentioned that by 2025, the company will have capacity of 11.5 MT through brownfield expansion. He estimates an overall capex of Rs 7,000 crore in case Orient Cement intends to expand capacity to 18 MTPA.

What also keeps the street interested is that Orient Cement's valuations are below $40 per tonne, again a sharp discount to its peers.

Shares of Orient Cement are down 6 percent so far this year. Over a 12-month period, the stock is down 23 percent.

(Edited by : Hormaz Fatakia)

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!

Dharwad Lok Sabha Election 2024: BJP's Pralhad Joshi eyes fourth term from this Karnataka seat

May 7, 2024 9:33 AM

Gulbarga Lok Sabha election: Mallikarjun Kharge's son-in-law Radhakrishna faces sitting BJP MP Umesh Jadhav

May 7, 2024 9:00 AM