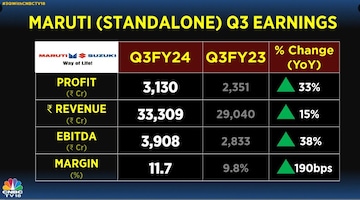

India's largest passenger car manufacturer Maruti Suzuki India saw its margin expand to 11.7% in the October to December 2023 quarter on the back of lower costs. Despite a sluggish industry growth outlook, brokerages see stronger margin tailwinds for the carmaker in the near term.

While brokerages have not revised their rating or target price on the auto stock, they see up to 23% upside in it from the closing price of January 31.

London-headquartered HSBC has a buy call on the Maruti Suzuki shares and set the target price at ₹12,500. The company performed well in a seasonally weak quarter, the brokerage said, adding that its margin should further improve with better operating leverage and fewer discounts.

“We believe 6-7% growth is possible for the company with margin expansion,” it said, adding that the industry growth is likely to remain sluggish in FY25.

Morgan Stanley, meanwhile, has an overweight stance on the company with a target price of ₹11,228 on the stock. It believes the firm is best placed to benefit from first-time buyer (FTB) recovery. It, however, pointed out the Hatch Plus Micro SUV segment is still running below FY19 levels.

Also, the brokerage said Q3 margin print points to upside risks to FY25 consensus margin estimates.

Nomura, on the other hand, has a neutral call on Maruti with a target price of ₹11,649. The brokerage lauded his steady performance. Even as it expects stronger margin tailwinds to sustain in the near term, it says the firm’s market share may face some risk in FY25-26.

The brokerage views come a day after the company reported its third-quarter results, in which its net profit came in at ₹3,130 crore, which is higher than the CNBC-TV18 poll projection of ₹3,050 crore.

Revenue for the quarter grew by 15% from last year to ₹33,309 crore, which was marginally lower than the CNBC-TV18 poll expectations of ₹33,744 crore. EBITDA or earnings before interest, tax, depreciation and amortisation grew by 38% from last year to ₹3,909 crore. The number was slightly lower than the ₹3,980 crore figure of the CNBC-TV18 poll.

(Edited by : Amrita)

First Published: Feb 1, 2024 8:46 AM IST

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!

Colour-coordinated theme-based polling booths set up in Srinagar

May 10, 2024 9:26 AM

Haryana: 16 women among 223 candidates in fray for 10 Lok Sabha seats

May 10, 2024 9:04 AM