Social media had a field day this week when Apple, the technology giant instrumental to transforming music devices and mobile phones, launched a cleaning cloth for USD 19.

Memes took over when Apple added a compatibility list to this product’s information – that is, the devices that ‘

the cloth’ can potentially clean. As if that weren’t enough in and of itself, a lot of us gasped when we realized that ‘the cloth’ is sold out until late November 2021!

Sounds bizarre, doesn’t it? A technology company launching a commodity cleaning product, at ten times the price of competition … and people lining up to buy it. It later dawned on me that it happens more often than we realise – and not just for consumer products, but everywhere, including with investments.

Daniel Kahneman, THE authority on behavioural economics, neatly sums up this bizarre behaviour with what he calls the ‘focusing illusion’. He says, "nothing in life is as important as you think it is, while you are thinking about it." When people believe that they "must-have" a good, they greatly exaggerate the difference the goodwill make to the quality of their life, he explains.

Kahneman asked a few people – given that the weather is beautiful in California – would they be happier if they lived there. Most people said yes. But when Kahneman asked Michiganders and others a different question (not focused on weather), they appeared just as contented as the Californians.

Relationships, work, and recreation are broadly similar no matter where one lives. Also, once you settle in a place, you do not think about the climate that much. When specifically prompted, however, ‘the weather’ assumes a bigger role in decision-making, simply because one is paying attention to it.

We can apply this framework to investments as well. We had argued in ‘

Discipline eats timing for lunch’ while people pay immense attention to timing the market, the difference in returns between disciplined investing and timing the markets is not large.

But when markets are galloping, all we focus is on how little we are invested in markets. And when it dramatically corrects, all we focus is on how we could have sold more. Because one constantly observes the market rises and falls, ‘timing’ assumes far more important than the fact that disciplined investing brings similar returns.

We had also argued disciplined investing works with individual stocks as well, provided one is in the right theme. Our focus is too often on timing the current theme ‘precisely’, rather than getting the next big trend ‘vaguely’ right.

In the third and final part, we take his line of thought forward. (a) Yes, discipline is far more important than timing (b) and yes, it must be in the right themes, but (c) today we argue that sector selection is of paramount importance.

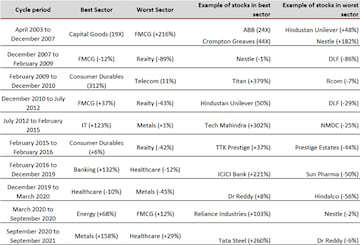

Let’s assume you are the Chief Investment Officer of a large Indian fund with total autonomy to run it as you deem fit. Between December 2007 and February 2009, your call on asset allocation (say debt vs. equity) would contribute close to 90 percent of the fund’s total returns.

The decision, then, to avoid Realty and invest in FMCG would contribute close to another 9 percent. Lastly, within FMCG, the decision on whether to invest in

ITC, or

Dabur, or

Nestle, in the overall scheme of things would be responsible for just 1 percent of your overall portfolio returns.

The table below lists the different market cycles in India with the best and worst returning sectors and relative performance of similar-sized businesses at that time.

Historically, sector selection has had a far larger impact on investment returns than stock selection within that sector. It is true that occasionally one embarks upon a company that cuts through these ‘sectoral cycles’ and outperforms across. But we focus an inordinate amount of time looking for those.

A great company in a sector that underperforms often generates many inferior returns to an average company belonging to a sector that outperforms.

But since we interact with, and focus on companies (stock prices, analyst calls, management calls) and not directly on sectors, we form the illusion that the right company is far more important than the right sector.

In what we consider a logical conclusion to the arguments we made over the

previous letters, we humbly submit that over the longer term, a focus on discipline, themes and sectors are likely to yield a far superior return than the illusion of timing the markets and getting the company selection right.

(Edited by : Yashi Gupta)