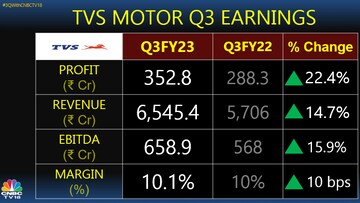

TVS Motor shares rose over four percent on Wednesday, a day after the two-wheeler maker reported its earnings for the October to December 2022 period in which its profit jumped 22 percent, slightly below estimates, and revenue rose close to 15 percent on a year-on-year basis.

Several brokerages raised the target price on the automaker, noting that its margin during the third quarter of the fiscal remained stable, driven by price hikes and commodity tailwinds.

Brokerage firm Goldman Sachs said the margin was stable despite improving average selling price. It added that the management was less concerned with uncertainty around the potential extension of the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme and that it is optimistic about a gradual recovery in two-wheeler demand.

TVS Motor remains UBS’ most preferred pick in two-wheelers. The brokerage expects iQube ramp-up to continue. It also noted that TVS credit performance was strong while exports bottomed out. The brokerage raised the target price to Rs 1,350 per share, implying a 26 percent upside in the stock from Tuesday’s closing price.

CLSA also raised its target price to Rs 971 as it maintained a cautious stance. According to the brokerage, strong Q3 was led by sharp QoQ increase in average selling price. The demand outlook looks uncertain in near term to the brokerage while it expects margin to expand as EV losses reduce, it said.

| Brokerage | Rating | Target price |

| Goldman Sachs | Neutral | Rs 1,050 |

| UBS | Buy | Rs 1,350 |

| CLSA | Sell | Rs 971 |

| Morgan Stanley | Equal-weight | Rs 1,121 |

| Jefferies | Buy | Rs 1,550 |

| Citi | Sell | Rs 800 |

Morgan Stanley pointed to in-line third quarter results despite weak volumes and said the firm maintained its margin driven by price hikes and commodity tailwinds. It expects the margin trend to continue in the near term. It eyes multiples at 22 for FY25 and added that EV disruption risks keep compel it to keep an equal-weight stance on the company.

Following the result, Jefferies highlighted that EBITDA per vehicle rose to a new high for the quarter. It believes that TVS should be a key beneficiary of Indian two-wheeler demand recovery. The firm is leading among incumbents in electric two-wheelers with 17 percent market share in January and plans to launch multiple products in the next 18 months, the brokerage said.

Citi, meanwhile, has a sell rating on TVS but has raised target price to Rs 800 per share. It sees there might be downward margin pressure as the proportion of EVs in the mix has increased.

The two-wheeler maker’s pricing power could be limited due to the onslaught of electric two-wheelers by competitors, the analyst said, adding that there could also be elevated competition in the domestic bikes segment market. It also said that export markets are challenged and that valuations at current levels provide limited room for error.

Check out our in-depth Market Coverage, Business News & get real-time Stock Market Updates on CNBC-TV18. Also, Watch our channels CNBC-TV18, CNBC Awaaz and CNBC Bajar Live on-the-go!

Surat polls: Congress moves EC claiming three proposers of party's candidate may have been abducted

Apr 23, 2024 12:59 PM

2024 Lok Sabha Election | How did Rahul Gandhi’s yatras strengthen I.N.D.I.A bloc’s prospects in South

Apr 23, 2024 9:57 AM

Nearly 26,000 teachers lose their job in Bengal — it may be significant turn in the Lok Sabha election

Apr 22, 2024 11:58 PM

Lok Sabha Elections phase 2: Battle of "guarantees" in Karnataka

Apr 22, 2024 11:15 PM